Forced Sale vs Quick Sale 2026 | What Should Property Owners Know?

A quick sale is usually a better option than a forced sale. In a quick sale, the price is often around 70–85% of market value. In a forced sale, it is often closer to 50–70%. Timing is also very different: a quick sale can take 7–30 days, while a forced sale may take 6–12 months or longer. A quick sale is private and remains under the owner’s control. A forced sale is a public process and may damage credit history for years. If you are at risk of a forced sale, it is worth considering a quick sale before the procedure goes too far.

Introduction

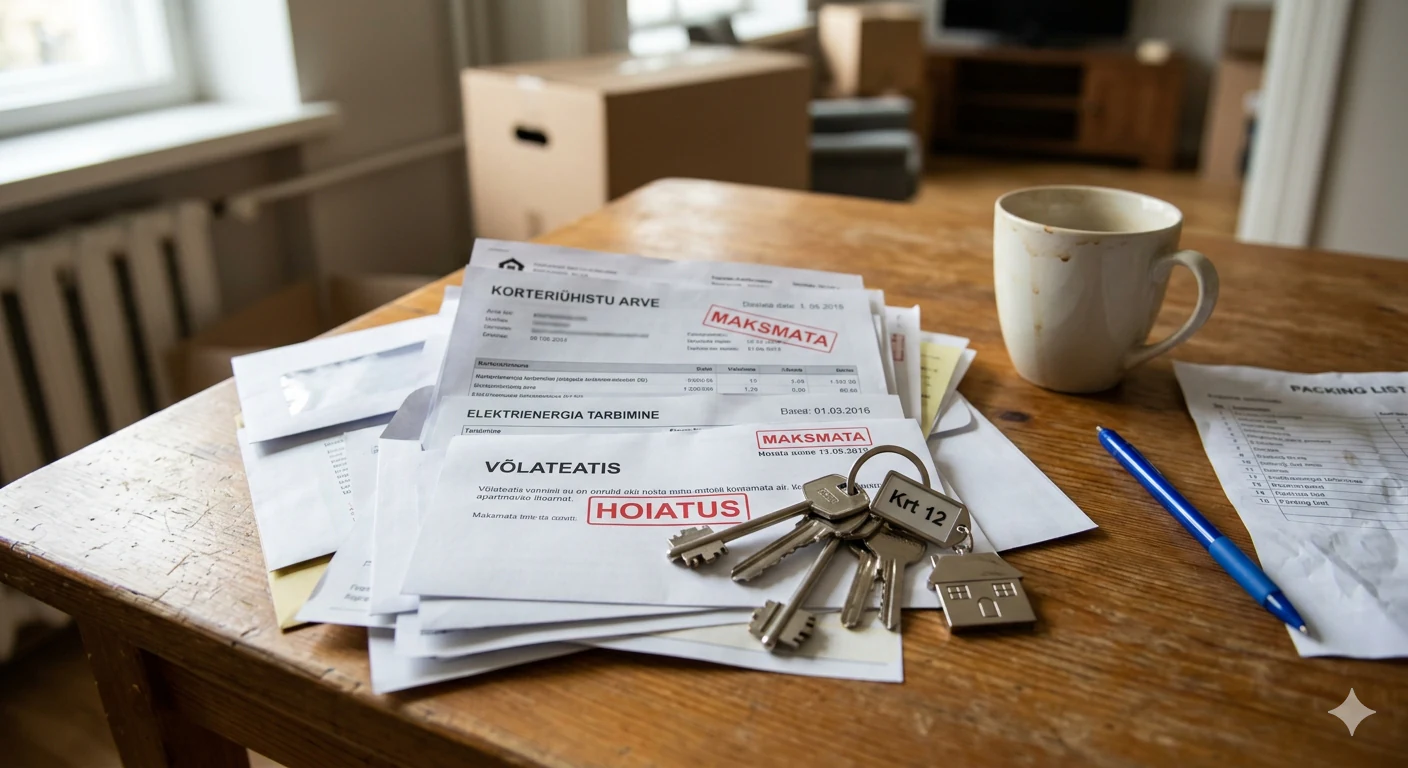

A forced sale is one of the most difficult situations for a property owner. It means the owner no longer has full control over the sale of the property. The process may be driven by creditors, a bank or an enforcement officer.

A quick sale is different. It is started by the owner. You decide whether to sell, who to sell to and what price you are willing to accept. The sale is faster than a standard property sale, but it is not a forced procedure.

This article compares forced sales and quick sales in practical terms: price, timeline, public visibility, credit history, costs and control over the transaction.

The main point is simple: if there is a risk of a forced sale, a quick sale may give you more control, a better price and a faster solution.

Important: If the forced-sale process has already started, not all options may be gone. In some cases, the property can still be sold before the auction, but you need to speak quickly with the creditor, the enforcement officer and a potential buyer.

What is a forced sale?

A forced sale is a property sale arranged through a court or an enforcement officer. It is usually used when the owner has not paid a debt and the creditor wants to recover the debt from the property.

A forced sale usually takes place:

to satisfy a debt claim;

after court proceedings or the start of enforcement proceedings;

through a public auction.

A forced sale may be initiated by, for example:

a bank, if mortgage payments have been unpaid for a long time;

an apartment association, if there is a large debt to the association;

the state or the Estonian Tax and Customs Board, if tax debt has arisen;

a private person or company, if they have a court-recognised claim.

Main stages of a forced sale

The creditor files a claim or starts debt collection.

The court makes a decision, or the claim moves into enforcement proceedings.

The enforcement officer starts the procedure and assesses the property sale.

The apartment is listed for public auction.

If the first auction fails, there may be a new auction with a lower starting price.

After the sale, the money is distributed among the creditors.

The whole process usually takes 6–12 months, but in more complex cases it can take longer.

What is a quick sale?

A quick sale is a voluntary way to sell a property faster than usual. The transaction often takes place within 7–30 days.

A quick sale can be useful when the owner needs to:

pay debts quickly;

avoid a forced sale;

move within a short time;

resolve a property issue related to inheritance or divorce;

sell without a long listing period and repeated viewings.

Quick sales are usually offered by:

direct buyers and property companies that buy properties for their own portfolio;

in some cases, estate agents or investors with an existing buyer network.

How a quick sale usually works

The owner decides that a fast sale is needed.

The owner asks one or more buyers for an estimate.

The buyer views the apartment and checks the main details.

The owner receives a concrete offer.

If the offer is acceptable, the parties sign a reservation or preliminary agreement.

The transaction is completed at a notary.

On average, this process takes 14–30 days. It can be faster in urgent cases if the documents are in order and all parties are ready to act.

Forced sale and quick sale: key differences

Aspect | Forced sale | Quick sale |

|---|---|---|

Who starts it | Creditor or enforcement officer | Owner |

Time | Usually 6–12 months | Usually 7–30 days |

Price compared with market value | Often 50–70% | Often 70–85% |

Visibility | Public auction | Private transaction |

Court involvement | Often required | Usually not required |

Control | The owner has little control | The owner decides |

Costs | Enforcement and procedural costs are added | Costs depend on the agreement |

Credit history | May be damaged for years | Usually not affected |

Stress | High | Usually lower |

Co-heirs or co-owners | Involvement may be forced | Involvement is based on agreement |

Forced sale

Who starts it

Creditor or enforcement officer

Time

Usually 6–12 months

Price compared with market value

Often 50–70%

Visibility

Public auction

Court involvement

Often required

Control

The owner has little control

Costs

Enforcement and procedural costs are added

Credit history

May be damaged for years

Stress

High

Co-heirs or co-owners

Involvement may be forced

Quick sale

Who starts it

Owner

Time

Usually 7–30 days

Price compared with market value

Often 70–85%

Visibility

Private transaction

Court involvement

Usually not required

Control

The owner decides

Costs

Costs depend on the agreement

Credit history

Usually not affected

Stress

Usually lower

Co-heirs or co-owners

Involvement is based on agreement

Difference 1: sale price

In a forced sale, the buyer often has a stronger position. The buyer knows the property is being sold under pressure. There may also be more risk: the apartment’s condition may be unclear, documents may be incomplete or handover may take time.

In a forced sale, a starting price is set for the auction. If there are few bidders, the apartment may sell far below market value. If the first auction fails, the starting price may be reduced at the next auction.

In a quick sale, the price is also usually lower than in a standard open-market sale because the buyer takes on speed, risk and resale or renovation costs. The difference is that the owner can accept or reject the offer.

Example:

Apartment | Market price | Possible forced-sale price | Possible quick-sale price | Difference |

|---|---|---|---|---|

Tallinn, Mustamäe, 50 m² | €130,000 | €78,000 (60%) | €104,000 (80%) | €26,000 |

Tartu, Annelinn, 65 m² | €110,000 | €66,000 (60%) | €88,000 (80%) | €22,000 |

Market price

Tallinn, Mustamäe, 50 m²

€130,000

Tartu, Annelinn, 65 m²

€110,000

Possible forced-sale price

Tallinn, Mustamäe, 50 m²

€78,000 (60%)

Tartu, Annelinn, 65 m²

€66,000 (60%)

Possible quick-sale price

Tallinn, Mustamäe, 50 m²

€104,000 (80%)

Tartu, Annelinn, 65 m²

€88,000 (80%)

Difference

Tallinn, Mustamäe, 50 m²

€26,000

Tartu, Annelinn, 65 m²

€22,000

These are examples, not guarantees. The actual price depends on the location, condition, documents, debt amount and market situation.

Difference 2: timeline

A forced sale moves slowly because creditors, the court, the enforcement officer and the auction process are involved. During this time, the owner may not know exactly when the sale will happen or what price the property will finally achieve.

Possible forced-sale timeline:

0–3 months: the creditor sends notices and tries to collect the debt;

3–6 months: the matter may move to court or enforcement proceedings;

6–9 months: the enforcement officer prepares the auction;

9–12 months: the sale takes place or a new auction is arranged.

A quick sale timeline is shorter and easier to manage.

Possible quick-sale timeline:

Day 1: first contact and sharing basic information;

Days 2–3: property viewing;

Days 4–5: concrete offer;

Days 5–7: reservation or preliminary agreement;

Days 10–14: notary transaction;

Days 14–17: money reaches the account.

The exact timing depends on the documents, the readiness of the parties and whether the apartment has a mortgage, tenants or other restrictions.

Difference 3: impact on credit history

A forced sale can have a serious impact on creditworthiness. If the matter reaches court or enforcement proceedings, it may leave traces in registers and in lenders’ risk assessments. This may later make it harder to get a home loan, leasing or other credit.

The impact can last for years. In practice, this may mean that a bank asks for more explanations, requires a larger down payment or rejects the loan application.

A quick sale is a normal voluntary transaction. If the debt is paid from the sale proceeds before the enforcement process escalates, it may be possible to reduce or avoid damage to credit history.

Difference 4: visibility and privacy

A forced sale is more public than a regular sale. Auction information may be visible in official channels, and people may find out about the situation even if the owner would prefer to keep it private.

A quick sale is more discreet. The transaction involves the owner, the buyer, the notary and, if needed, the bank or other related parties. There is no need for a public listing, and the owner does not have to arrange viewings for dozens of buyers.

This matters especially when the owner wants to resolve debt, divorce, inheritance disputes or another sensitive situation quietly.

When can a forced sale be unavoidable?

A forced sale cannot always be avoided. In some cases, the situation is already too far advanced or the parties cannot reach an agreement.

1. Several creditors with conflicting interests

If there are several claims and the creditors do not agree on a solution, a forced sale may be the only way to sell the property and distribute the money.

2. Inheritance or co-ownership dispute

If heirs or co-owners cannot agree on the sale, the solution may have to come through the court.

3. The procedure is already far advanced

If the auction has already been announced or is about to take place, there may be too little time to arrange a voluntary sale.

Even in these cases, it is worth checking whether a direct sale is still possible. If the buyer can act quickly and offer a better result than the expected auction outcome, the creditor and enforcement officer may in some cases agree.

How can a quick sale help avoid a forced sale?

The earlier you act, the more options you have.

If the bank has sent warnings

Stage 1: payment is 1–3 months late

The bank sends reminders. At this stage, you should contact the bank immediately. You may be able to ask for a payment holiday, a changed payment schedule or another temporary solution.

Stage 2: the debt has lasted 3–6 months

The bank may start taking more serious steps. At this point, a quick sale is already a realistic option. The owner can find a buyer and use the sale proceeds to repay the debt.

Stage 3: court or enforcement proceedings have started

There is less time, but an option may still exist. You need a buyer who can act quickly and an agreement with the bank or another creditor.

Stage 4: the enforcement officer is handling the sale

If the auction has not yet taken place, a direct sale may still be possible in some cases. This requires the consent of the enforcement officer and the creditor.

Practical action plan

Today:

contact one or more quick-sale buyers;

be honest about the situation: debt amount, bank, and the stage of court or enforcement proceedings;

ask for an initial estimate.

Next 2–3 days:

allow the buyer to view the apartment;

get a concrete offer in writing.

Next 4–7 days:

speak with the bank or creditor;

ask whether they will agree to a direct sale if the debt is paid from the sale proceeds;

involve the enforcement officer if needed.

Within 7–14 days:

formalise the agreements;

move to the notary transaction;

pay the debt from the sale proceeds.

A bank often prefers a fast and clear solution if it gives a better result than a long forced-sale process.

If a forced sale cannot be avoided

If a forced sale is unavoidable, it is still useful to know what is happening and what rights you have.

What can you do?

You can:

ask for information about the status of the procedure;

review the valuation and auction terms;

challenge the valuation if it seems clearly unreasonable;

look for a buyer yourself, if the enforcement officer and creditor allow it;

seek advice from a lawyer or debt adviser.

You should not:

obstruct the auction if the procedure is legally underway;

sell the property secretly to a third party;

remove important items or equipment from the apartment if this breaches agreements or procedural terms;

ignore letters from the enforcement officer.

What happens after the sale?

After the sale, the money is usually distributed in this order:

enforcement and procedural costs are paid;

creditors are paid according to their claims and priority;

any remaining amount is paid to the owner.

If the debt, interest and costs are large and the sale price is low, there may be nothing left for the owner.

Frequently asked questions

How large is the price difference between a forced sale and a quick sale?

The typical difference may be 15–25 percentage points. In a forced sale, the price may be around 50–70% of market value, while in a quick sale it is often around 70–85%. For a €100,000 apartment, this may mean a difference of €15,000–25,000.

Can a quick sale prevent a forced sale if court proceedings have already started?

Often it can, but it depends on the stage of the procedure. You need the creditor’s consent, a buyer who can act quickly and, in some cases, cooperation from the enforcement officer.

What happens to credit history after a forced sale?

A forced sale and the related procedure can seriously affect creditworthiness. The impact may last several years and make it harder to obtain a new home loan, leasing or other credit.

Can the owner receive money after a forced sale?

Yes, but only if the sale price covers all debts, interest and procedural costs. If any money remains after these have been paid, it is transferred to the owner. In practice, there may not always be a surplus.

Can a forced sale be stopped or cancelled?

Before the procedure ends, it may be possible if the debt is paid or an agreement is reached with the creditor. Once a court decision has entered into force and the auction is approaching, there are fewer options and action must be taken quickly.

How long does a forced sale take?

On average, 6–12 months, but disputes, appeals or failed auctions can make the process longer.

Why do quick-sale buyers offer less than the normal market price?

A quick-sale buyer pays for speed and certainty. They take on some of the risks, transaction preparation, possible repairs, resale work and capital cost. For that reason, the price is lower than market price, but the transaction happens faster.

Is avoiding a forced sale always better?

Usually yes, but every situation is different. If the debt is small or the sale creates other risks, it is worth speaking with a lawyer, debt adviser or financial adviser before deciding.

Can the owner find a buyer during forced-sale proceedings?

Sometimes yes. You need to speak with the enforcement officer and the creditor. If the buyer offers a better result than the expected auction, a direct sale may be more reasonable for everyone.

How can you find a trustworthy quick-sale buyer?

Check whether the buyer or company is registered in the business register. Ask about previous transactions, read reviews and request the contract terms in writing before signing. A trustworthy buyer explains the offer and does not pressure you to decide before you understand the terms.

Summary

If you are at risk of a forced sale, a quick sale is worth serious consideration. It is not suitable for every situation, but it often gives the owner more control and a better outcome.

Metric | Quick sale | Forced sale | Possible benefit for the owner |

|---|---|---|---|

Price | 70–85% of market value | 50–70% of market value | +15–25 percentage points |

Time | 7–30 days | 6–12 months | much faster |

Credit history | Usually preserved | May be damaged for years | lower risk |

Control | Owner decides | The procedure controls the sale | more decision-making power |

Stress | Lower | High | clearer process |

Quick sale

Price

70–85% of market value

Time

7–30 days

Credit history

Usually preserved

Control

Owner decides

Stress

Lower

Forced sale

Price

50–70% of market value

Time

6–12 months

Credit history

May be damaged for years

Control

The procedure controls the sale

Stress

High

Possible benefit for the owner

Price

+15–25 percentage points

Time

much faster

Credit history

lower risk

Control

more decision-making power

Stress

clearer process

Important time windows:

Before court or enforcement proceedings: the most options.

During proceedings: an option may still exist, but action must be quick.

After the enforcement officer is involved: possible only by agreement.

Right before the auction: options are limited.

Need help avoiding a forced sale?

We have experience with debt-related and complex property transactions. We can help assess whether a quick sale could be a reasonable solution in your situation.

We offer:

✓ a free initial consultation — we discuss your situation discreetly;

✓ a fast estimate — we provide an initial response quickly;

✓ help communicating with the bank or enforcement officer — if needed;

✓ a fast transaction — the goal is to reach the notary as smoothly as possible.

Fill in the form and get an offer

Read More

Apartment with debt 2026 | How to avoid a forced sale

Have debts attached to your apartment? Learn how to sell before a forced sale and settle creditors during the transaction.

Read more

Selling an apartment when moving abroad 2026

Moving to Finland, Germany or elsewhere? See how to sell an apartment before or after leaving Estonia, how a notarised power of attorney works and how to transfer the money abroad.

Read more

Property fast-sale price 2026 | How is it calculated?

How is the fast-sale price of an apartment calculated? A clear formula and examples from Tallinn and Tartu. Request an offer today!

Read more