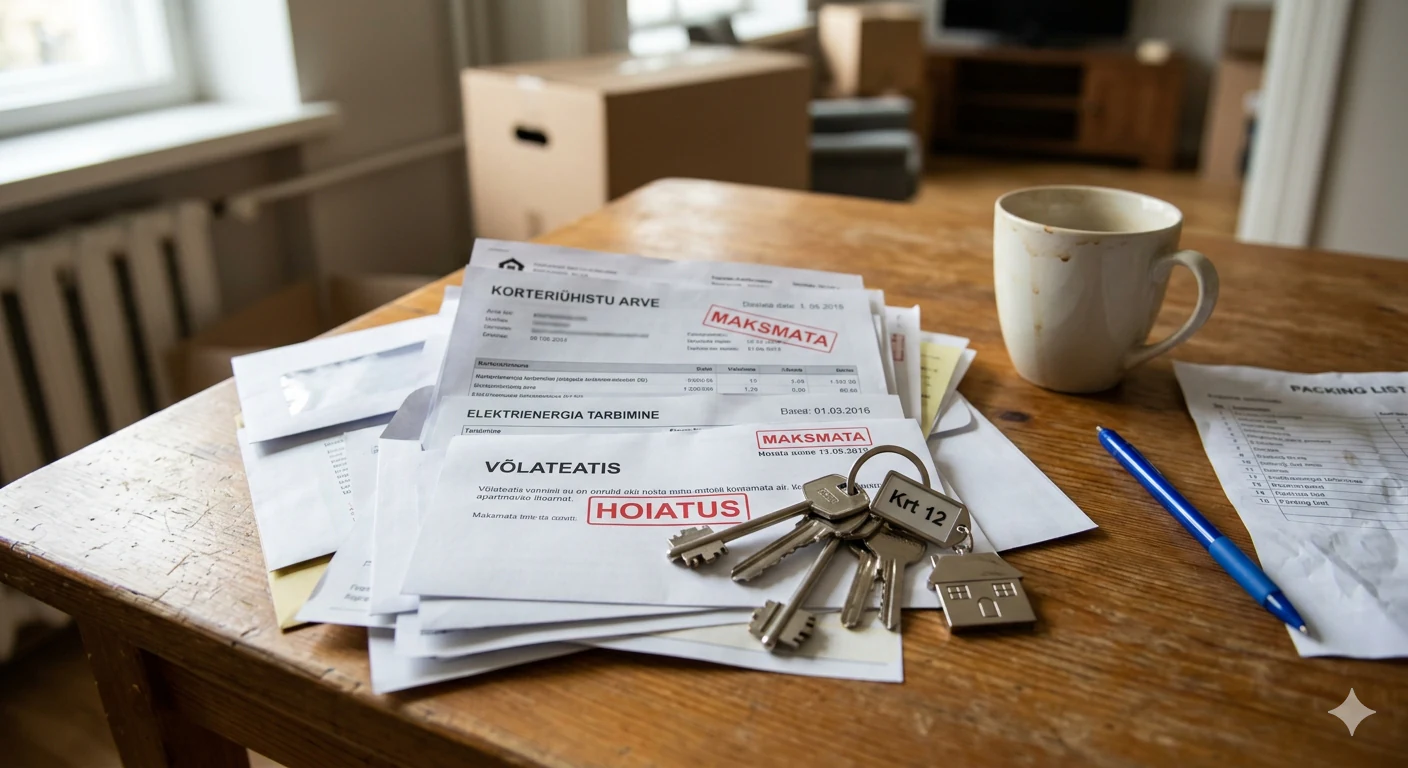

Apartment with debt 2026 | How to avoid a forced sale

In brief

If debts are connected to your apartment, it is usually better to act before the situation reaches a forced sale. A voluntary sale often gives the owner more control, a better price and a clearer timeline.

An apartment sale can be affected by a home loan, apartment association debt, a bailiff's seizure, tax debt or other claims. During the sale, some or all debts can often be paid directly from the purchase price. The exact order depends on mortgages, seizures, creditors' claims and the terms agreed at the notary.

The sooner you map out the situation, the more options you usually have.

Introduction

Selling an apartment with debts is uncomfortable, but it is not rare. Higher interest rates, rising living costs and changes in income have put many families under pressure. The main thing is not to wait until the problem grows.

This article explains which debts can affect the sale of an apartment, how to prepare for the sale and what to do if creditors are already involved. We also look at how to avoid a forced sale and which documents are usually needed.

Important: the situations below are general examples. Every case depends on the documents, the creditors and the entries in the Land Register. If the debt is large or a bailiff is already involved, it is worth speaking with a lawyer or debt adviser.

Which debts can affect the sale of an apartment?

1. Home loan and mortgage

What it is: a bank loan secured by your apartment.

How it affects the sale:

an apartment can be sold even if it has a mortgage;

the outstanding loan balance is usually paid from the purchase price;

the bank's conditions and consent are needed to remove the mortgage;

if the sale price does not cover the loan balance, the missing amount must be covered in another way or agreed separately with the bank.

2. Debt to the apartment association

What it is: unpaid utility, maintenance or management fees owed to the apartment association.

How it affects the sale:

the association can demand payment and, if needed, go to court;

a larger debt can slow down the transaction or reduce the buyer's offer;

buyers and notaries often ask for a certificate showing whether there are debts to the association;

the debt can usually be paid from the purchase price during the notary transaction.

The debt may range from a few hundred euros to several thousand euros. The exact amount depends on the building, monthly costs and how long the payments have been overdue.

3. Seizure by a bailiff

What it is: a bailiff has placed a seizure on the property to collect a debt.

How it affects the sale:

a seizure can prevent a standard sale transaction;

a sale may still be possible if the bailiff and the required parties give consent;

the claims related to the seizure are paid from the purchase price in the agreed order;

a voluntary sale can lead to a better outcome than an auction.

4. Tax debt

What it is: unpaid taxes or other claims owed to the state.

How it affects the sale:

tax debt can lead to enforcement proceedings or seizure;

before the transaction, it must be checked whether the claim appears in the Land Register or in enforcement proceedings;

consent from the Tax and Customs Board or a bailiff may be needed for the sale.

5. Consumer loans, credit card debt and collection claims

What it is: payday loans, credit card debt, hire purchase debt or claims handled by a collection agency.

How it affects the sale:

these debts do not block the sale if no seizure has been placed on the apartment;

if the claim has reached court or enforcement proceedings, it may affect the sale;

before selling, it is worth checking whether there are any seizures or restrictions in the Land Register.

How does a sale work when debts are involved?

Step 1: gather exact information about the debts

Before looking for a buyer, you need to know how serious the situation is.

Write down the following for each debt:

the creditor's name;

the current debt amount;

interest and extra costs;

how many months the payments are overdue;

whether the matter is in court or with a bailiff;

whether a seizure has been placed on the apartment.

Where to get the information:

from the bank — the loan balance and the conditions for removing the mortgage;

from the apartment association — a debt certificate;

from the Land Register — mortgages, seizures and other entries;

from the bailiff or collection agency — the exact claim amount and the status of the proceedings.

Step 2: check whether the sale will cover the debts

The main question is simple: will the expected sale price cover the loan, seizures, apartment association debt and other claims?

Example where selling makes sense:

Market value of the apartment: €130,000 Expected quick-sale price: €104,000 Debts: - home loan: €70,000 - apartment association debt: €1,500 - bailiff's claim: €5,000 Total: €76,500 Amount left after paying debts: €104,000 - €76,500 = €27,500

In this example, the sale covers the debts and part of the money remains for the seller.

Example where the sale price does not cover everything:

Market value of the apartment: €100,000 Expected quick-sale price: €80,000 Debts: - home loan: €70,000 - apartment association debt: €3,000 - bailiff's claims: €15,000 Total: €88,000 Shortfall: €80,000 - €88,000 = -€8,000

In this case, the shortfall must be covered in another way or negotiated with the creditors.

Step 3: speak with creditors before the transaction

If the apartment has a mortgage, seizure or significant debt, do not wait until the day of the notary appointment. The terms should be discussed with the creditors in advance.

With the bank:

ask for the exact loan balance;

find out on what terms the bank will agree to remove the mortgage;

ask how quickly the bank can issue the consent needed for the transaction.

With the apartment association:

ask for a current debt certificate;

agree that the debt will be paid during the notary transaction;

ask the association to confirm the exact amount it expects to receive.

With the bailiff:

explain that you want to sell the apartment voluntarily;

ask which documents and consents are needed;

clarify how the purchase price will be divided between the claims.

Step 4: find a buyer who can act quickly

When debts are involved, time is often important. A suitable buyer should be able to make a decision quickly, work with the documents and complete the transaction at the notary.

It helps if the buyer:

can make an offer quickly;

understands transactions involving mortgages and seizures;

does not need a long bank process;

keeps the transaction discreet.

Step 5: the notary transaction

At the notary, the parties agree how the purchase price will move and which debts will be paid from it.

Usually it works like this:

the buyer transfers the money to the notary's deposit account or pays in another agreed way;

the notary arranges payments according to the transaction terms;

payments are made to the bank, bailiff, apartment association or other parties;

after the agreed obligations are paid, the remaining amount is transferred to the seller.

Step 6: after the transaction

After the notary appointment, payments may take a few business days. The exact timing depends on the bank, the notary and the number of parties involved.

Once all claims are settled, the required entries can be removed and the seller receives the remaining money.

Who gets paid first from the purchase price?

There is no single order that applies to every case. It depends on the entries in the Land Register, the type of claims and the agreements between the parties. In practice, the following obligations are usually reviewed:

Obligation | What it means |

|---|---|

Mortgage to the bank | The bank has security over the apartment. The loan balance usually has to be paid so the mortgage can be removed. |

Bailiff's seizures | Seizures must be resolved before ownership can pass freely. |

Tax debts | If a tax debt is in enforcement proceedings or registered as a seizure, it must be taken into account. |

Apartment association debt | The buyer and notary will want to know whether the apartment has any debt to the association. |

Other creditors | Their claims depend on whether they have reached enforcement proceedings. |

Amount left for the seller | The seller receives money after the agreed obligations have been paid. |

- Obligation

Mortgage to the bank

- What it means

The bank has security over the apartment. The loan balance usually has to be paid so the mortgage can be removed.

- Obligation

Bailiff's seizures

- What it means

Seizures must be resolved before ownership can pass freely.

- Obligation

Tax debts

- What it means

If a tax debt is in enforcement proceedings or registered as a seizure, it must be taken into account.

- Obligation

Apartment association debt

- What it means

The buyer and notary will want to know whether the apartment has any debt to the association.

- Obligation

Other creditors

- What it means

Their claims depend on whether they have reached enforcement proceedings.

- Obligation

Amount left for the seller

- What it means

The seller receives money after the agreed obligations have been paid.

Important: if the sale price does not cover all debts, not every creditor may receive the full amount. Separate agreements may then be needed.

What if the sale price does not cover all debts?

This can happen if the apartment's value has fallen, the debts have grown or several seizures have been placed on the apartment. The options depend on the creditors and the size of the shortfall.

Option A: agreement with creditors

Sometimes it is possible to agree that part of the debt is paid immediately and the rest later under a payment schedule. If the sale gives the creditor a better result than a forced sale, the creditor may be willing to negotiate.

Option B: sale with creditor consent

If the sale price is lower than the total debt, separate consent from the bank or other creditors may be needed. This is sometimes called a short sale, but in Estonia it depends mainly on the specific agreements.

Option C: covering the shortfall yourself

If the shortfall is small, it may be covered from savings, with help from family or through a separate payment schedule.

Option D: personal bankruptcy or debt restructuring

If the debts are larger than the assets and your income is not enough to pay them, it may be necessary to discuss personal bankruptcy or debt restructuring with a debt adviser or lawyer. This is a serious step and does not suit every situation.

Option E: postponing the sale

Sometimes it may make sense to wait and try to bring the payments back under control. The risk is that the creditor may start enforcement proceedings or a forced sale in the meantime. If that happens, the owner usually has less control.

How to avoid a forced sale

A forced sale is usually the last stage. It can often be avoided if you act before the creditor has gone too far with the proceedings.

The usual path before a forced sale

1. Late payments

The bank or another creditor sends reminders. At this stage, contact them right away and ask about a payment holiday, payment schedule or another solution.

2. Debt collection

If payments are not made, the debt may move to a collection agency or to court. This is a good time to get advice and assess whether a voluntary sale could prevent greater loss.

3. Court or enforcement proceedings

If the claim reaches court or a bailiff, selling becomes more complicated, but not always impossible. It is important to act quickly and obtain written consents.

4. Auction

If the apartment is put up for auction, the owner loses much of the control over price and timing. This is why a voluntary sale is often the better solution.

Common situations

Situation 1: the apartment association is claiming the debt in court

The apartment association is claiming, for example, a €4,000 debt and the owner cannot pay it all at once.

Possible solution:

contact the association and ask for a payment schedule;

if a payment schedule is not possible, consider selling the apartment before the proceedings go further;

agree that the association debt will be paid during the notary transaction.

Situation 2: the bank threatens to terminate the loan agreement

Several monthly payments are overdue and the bank may demand payment of the full loan balance.

Possible solution:

speak with the bank immediately, not after the next letter;

ask for a payment holiday, a change to the schedule or time for a voluntary sale;

show the bank a realistic plan for paying the debt from the sale.

Situation 3: the apartment has several seizures

Several claims are connected to the apartment, for example a private claim, tax debt and a collection claim.

Possible solution:

identify all claims and their exact amounts;

communicate with the bailiff and creditors;

if needed, use a lawyer so the transaction is clear for all parties.

Situation 4: a forced sale is close

There is already a court decision and the bailiff is preparing an auction.

Possible solution:

contact the bailiff immediately;

ask whether a voluntary sale is still possible;

if you find a buyer who offers a better result than the expected auction outcome, it may be more reasonable for everyone involved.

Frequently asked questions

Can I sell an apartment if it has a mortgage and apartment association debt?

Yes, in most cases you can. The transaction must take into account both the bank's conditions and the association debt. These are usually paid from the purchase price during the notary transaction.

What happens if the sale price does not cover all debts?

You need to negotiate with the creditors. Possible solutions include a payment schedule, paying part of the debt from the sale, covering the shortfall yourself or, in more difficult cases, debt restructuring.

Can I choose who gets paid first?

Not always. The order depends on mortgages, seizures, the type of claims and the transaction terms. The notary and, if needed, a lawyer can review this before the transaction.

How long does it take to pay the debts after the sale?

Payments usually move within a few business days after the notary transaction. The exact time depends on the bank, the notary and the creditors.

Can I sell an apartment if it has been seized by a bailiff?

Often yes, but the bailiff's consent is needed. A sale involving a seizure must be agreed in detail before the transaction.

Should I inform creditors before accepting an offer?

Yes, it is sensible. If the bank, bailiff or apartment association has a role in the transaction, early communication helps avoid delays.

What is a short sale?

A short sale means that the property is sold for a price that does not cover the full debt, and the creditor agrees to it. In Estonia, this depends on the specific agreements between the parties.

Can I pay creditors less in a quick sale?

Not automatically. A quick sale mainly means a faster transaction. Any reduction or rescheduling of debt requires a separate agreement with the creditor.

Is personal bankruptcy better than a quick sale?

Usually not. Bankruptcy or debt restructuring is a serious step and only makes sense when other solutions do not work. Before making that decision, get professional advice.

What happens if I ignore the debts?

The debt can grow because of interest, penalties and enforcement costs. Court proceedings, enforcement proceedings or a forced sale may follow. The longer you wait, the fewer good options you usually have.

Summary

If debts are connected to your apartment, the most important thing is to get a clear overview and act before a forced sale begins.

Keep in mind:

list all debts, claims and register entries;

ask the bank, apartment association and bailiff for current amounts;

check whether a sale will cover the obligations;

speak with creditors before going to the notary;

ask for help from a lawyer or debt adviser if needed.

What to do today:

☐ gather the creditors' contact details;

☐ ask for exact debt amounts;

☐ check the Land Register entries;

☐ estimate a realistic sale price for the apartment;

☐ contact a buyer who can act quickly;

☐ consider a payment schedule or an agreement with the bank if selling is not the best option.

Need confidential help selling an apartment with debts?

We have helped apartment owners in situations where the sale is affected by a loan, apartment association debt, seizure or another claim.

We offer:

✓ A free consultation — we review the situation calmly;

✓ A realistic assessment — even if selling is not the best choice;

✓ Help communicating with creditors — with your permission;

✓ A quick transaction — if the documents and consents are in order;

✓ Discretion — without a public listing;

✓ A free valuation within 24 hours.

Fill in the form and get an offer

Read More

Selling an apartment when moving abroad 2026

Moving to Finland, Germany or elsewhere? See how to sell an apartment before or after leaving Estonia, how a notarised power of attorney works and how to transfer the money abroad.

Read more

Property fast-sale price 2026 | How is it calculated?

How is the fast-sale price of an apartment calculated? A clear formula and examples from Tallinn and Tartu. Request an offer today!

Read more

Selling an Old Apartment Without Renovating in 2026 | Guide

Want to sell an old apartment without renovating it first? It is possible. Khrushchevka, Brezhnevka or any apartment that needs work — here is when renovation makes sense and when it does not.

Read more